After a whirlwind run of eye-popping M&A transactions last year, 2025 could be a year of reset for the upstream sector.

Unlike in 2024, few obvious combinations in U.S. shale basins stand out to analysts. The best acreage in the mighty Permian Basin is mostly accounted for, locked up in the portfolios of some of the world’s largest oil producers.

The growth engines for other key Lower 48 plays—the Williston, the Eagle Ford, the Denver-Julesburg (D-J)—have sputtered and transitioned into long plateaus.

More emerging plays, like Utah’s Uinta Basin and the Ohio Utica oil window, are showing upside, but they are dwarfed by the Permian.

E&Ps seeking a longer runway in U.S. shale in 2025 will need to get creative, said Andrew Dittmar, director at Enverus Intelligence Research.

“I think it’s going to be a tough market for buyers in ‘25 in terms of finding assets,” Dittmar told Oil and Gas Investor, “whether you’re looking in the Permian or elsewhere.”

RELATED

Shale Consolidation Aftermath: The Field Narrows

Priced out of paradise

Every E&P wishes it had more Permian Basin drilling locations.

Permian wells have some of the lowest breakeven costs of any U.S. shale play. Layers and layers of stacked pay give producers many shots on goal to co-develop multiple benches. Permian-heavy E&P names boast higher market values and trading multiples in the public markets.

Producers big and small clamor for a bigger slice of the Permian, the nation’s only real driver of oil output growth, but asking prices for Permian assets are sky high. That’s leading some cost-conscious producers to turn away from the basin and look elsewhere for new value.

SM Energy, Ovintiv and Devon Energy illustrated this trend in the back half of 2024.

Each of those E&Ps were rumored to be on the hunt for new Permian acquisitions—part of a broader M&A wave sweeping across the sector.

Ultimately, each company decided to spurn high Permian prices in favor of more compelling returns in other basins.

Instead of doubling down on the Midland Basin, SM Energy set its sights on the Uinta Basin. SM teamed up with non-operated partner Northern Oil and Gas (NOG) to acquire leading Uinta producer XCL Resources for $2.6 billion.

SM acquired an 80% undivided interest in XCL’s assets for $2.1 billion, while NOG picked

up the remaining 20% non-op stake.

Building on the Uinta M&A momentum, Ovintiv decided to sell its Uinta assets for $2 billion to FourPoint Resources, a privately-held E&P.

Instead of buying Double Eagle IV in the Permian, Ovintiv decided to enlarge its presence in Canada’s Montney Shale through a US$2.38 billion (CA$3.33 billion) deal with Paramount Resources.

Despite their expansions in the Permian, both companies opted to take a breather from the Permian’s high prices and look outside the basin for value, said Matthew Bernstein, vice president and manager of upstream solutions for Rystad Energy.

Devon Energy was also rumored to be scouring the Permian for deals when it announced a $5 billion acquisition of Grayson Mill Energy in the Williston Basin.

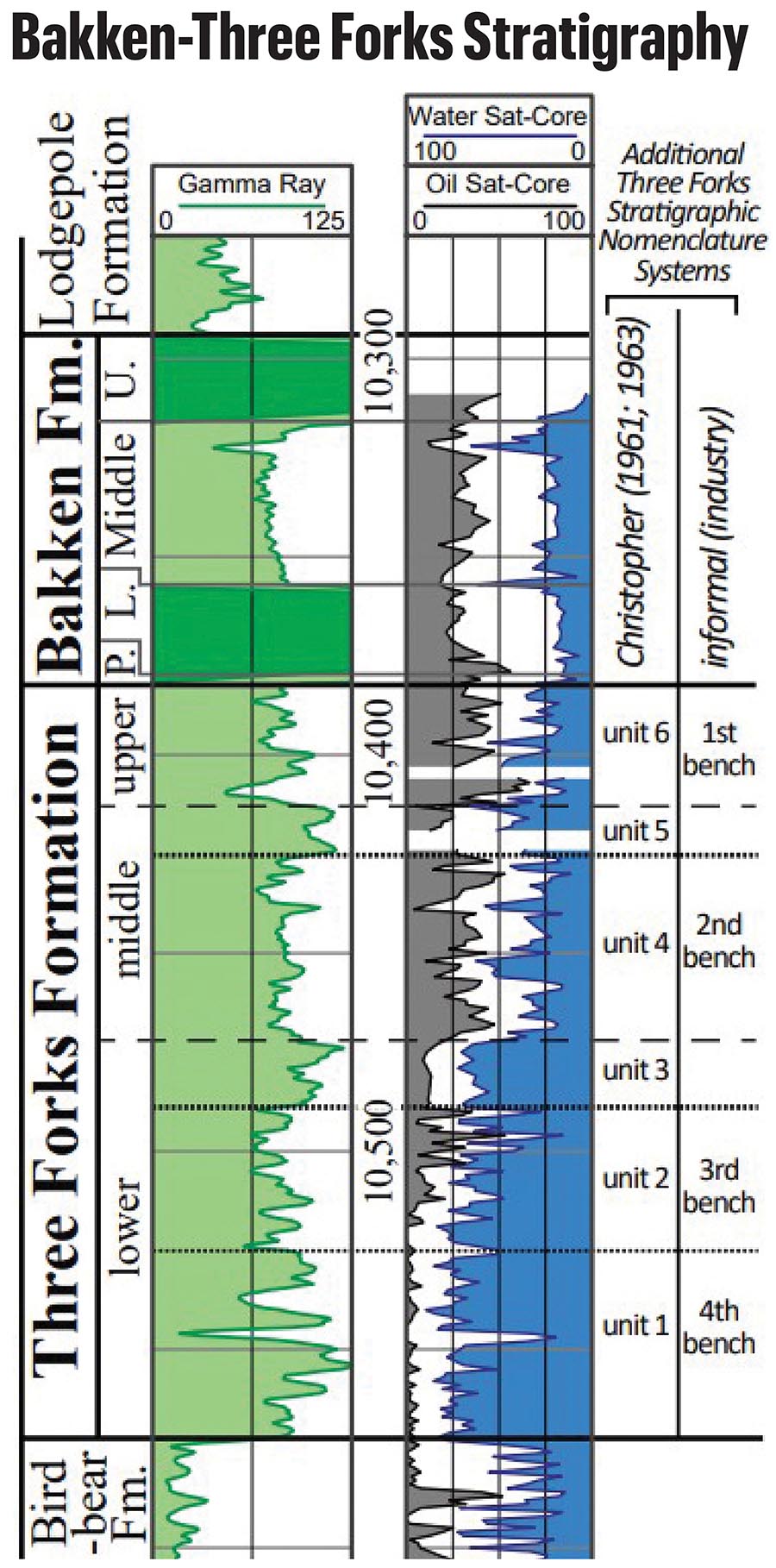

The Grayson Mill deal added 500 gross undrilled Williston locations, and around 300 candidates for potential refrac projects. Around 80% of the new locations were in the Bakken Shale, the remaining 20% in the deeper Three Forks benches.

“As those Permian assets get a bit more expensive, a bit riskier and harder to come by, you do see more companies being willing to look at other basins,” Dittmar said.

“The unfortunate part is there’s not a whole lot to find in those, either,” he said. “It’s not like there’s a plethora of assets to go buy in the Eagle Ford or the Williston.”

Enverus forecasts that 2025’s M&A environment will include smaller deals and deals further up the cost curve, or looking at less economic, lower-tier rock, Dittmar said.

RELATED

Anschutz Explores Utah Mancos Shale Near Red-Hot Uinta Basin

Williston runway

The Williston Basin of North Dakota and eastern Montana lacks the growth profile of the Permian. Production from the mature Williston Basin actually shows signs of plateauing and declining, Williston wildcatter Harold Hamm told OGI late last year.

Williston operators are focusing on drilling more efficiently and lowering their costs instead of growing output at a breakneck pace. Producers are optimizing development of the Williston’s secondary benches, the Three Forks zones, which underly the shallower Bakken Shale.

Historically, the Middle Bakken has been the Williston Basin’s top drilling target. Williston operators like Hamm’s Continental Resources began landing laterals in the upper Three Forks as geologic understanding of the play grew over time.

But new research suggests major undeveloped upside remains in deeper parts of the Three Forks bench.

Operators had only landed 40 laterals in the middle (second) and lower (third) Three Forks benches through August 2023, according to studies published by the North Dakota Department of Mineral Resources.

That represents only around 2% of total drilling activity in the entire Williston Basin, authors Timothy Nesheim and Edward Starns reported.

But data collected from 25 drilling spacing units (DSUs) shows co-development of the middle Three Forks bench “exhibited a clear volumetric addition of oil” compared to DSUs without middle Three Forks wells.

Not counting existing wells, another 604 middle Three Forks horizontals could still be drilled within the core of the Williston Basin, according to the study. Ultimate EURs for the new projects could range between 165 MMbbl and 410 MMbbl of oil.

Williston operators are also combining land positions to drill longer laterals underground.

Devon plans to sustain production from the acquired Grayson Mill asset at around 100,000 boe/d this year through a mix of 2- and 3-mile laterals, as well as “tactical refracs” to supplement the base output, Devon COO Clay Gaspar said during the company’s third-quarter earnings call.

“The Williston Basin has been a tremendous provider of energy for a long time,” said William Westler, Rockies business unit vice president for Devon, in a statement to OGI. “We are excited and confident that the Grayson Mill acquisition allows us to continue to expand our production and operating scale with additional highly economic drilling inventory in the Williston for years to come.”

After closing a $4 billion acquisition of fellow Williston operator Enerplus, Chord Energy planned to drill more 3-mile wells and aimed to begin drilling 4-mile Bakken laterals.

Formentera Energy Partners, founded by partner Bryan Sheffield, is watching nearby operators drill 3- and 4-mile laterals from its position in Divide County, North Dakota, Sheffield said at Hart Energy’s Energy Capital Conference in October.

“Particularly in the Williston,” Dittmar said, “being able to go from a 2-mile to a 3-mile lateral knocks about $5 off your breakeven.”

Despite the runway to be had in the Williston, there aren’t many obvious places to go after it. The acquisitions of Grayson Mill and Enerplus plucked two large Williston positions from the drawing board.

The $17.1 billion merger of ConocoPhillips and Marathon Oil also consolidated huge swathes of Williston Basin acreage.

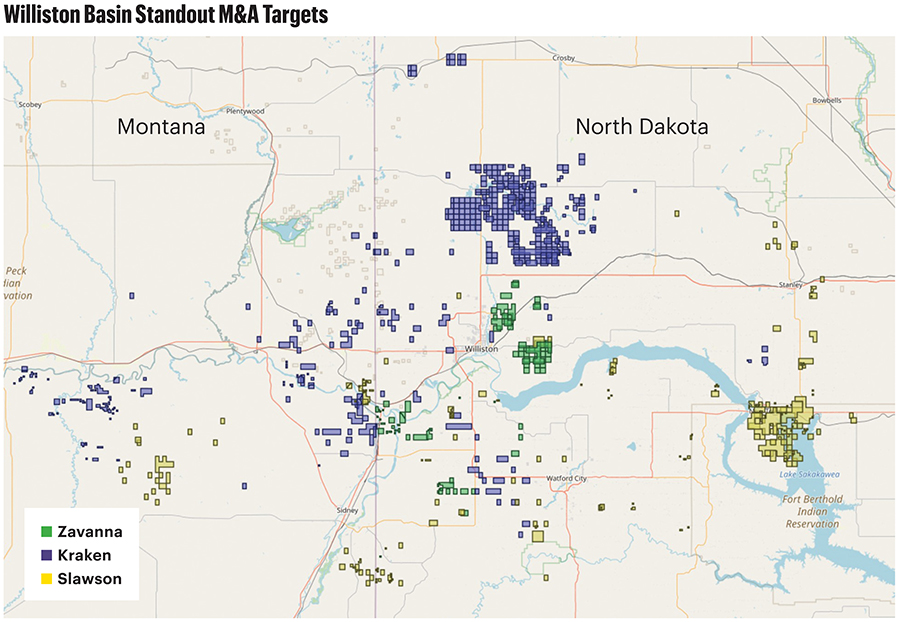

Williston producers of notable scale that could be potential sellers include Kraken Resources, Slawson Exploration and Zavanna LLC.

Private equity firm Carnelian Energy Capital invested in Zavanna last fall. The company has around 150 drilling locations across the Bakken and Three Forks.

RELATED

Analysis: Middle Three Forks Bench Holds Vast Untapped Oil Potential

Eagle Ford flies

A growing list of Eagle Ford operators are leaning into refracs, re-entries, recompletions or other re-do jobs to breathe new life into legacy wells with declining production.

Eagle Ford producers touting refrac projects include ConocoPhillips, Devon, BPX Energy, Crescent Energy, Baytex Energy and Verdun Oil, among others.

Refracs are a hot topic today. For Verdun Oil, backed by private equity firm EnCap Investments, they’re old news.

Verdun started developing a refrac strategy around 2018, when the company completed what it says was the first full linear isolation refrac job performed in the Eagle Ford trend.

A cemented linear refrac involves installing a new liner inside the wells’ existing casing, which covers all the previous fracs. Then, the well is fracked as if it were a new project.

The other main type of refrac—bullhead refracs—do not direct frac fluid and are less costly alternatives to a full linear isolation refrac project.

Not every well makes sense for a refrac. The wells Verdun has singled out for refracs generally have lateral lengths of around 6,000 ft and were completed prior to 2016.

M&A horizon

Like the Williston, the Eagle Ford holds fewer obvious combinations through potential M&A.

The merger between ConocoPhillips and Marathon Oil brought together two of the largest Eagle Ford producers.

The Marathon deal added around 1,000 Eagle Ford locations to ConocoPhillips’ portfolio. The companies have touted an even longer Eagle Ford runway, including potential refracs in the play.

Crescent Energy has been an active consolidator in the southern and central Eagle Ford. In its largest deal last year, Crescent closed a $2.1 billion acquisition of SilverBow Resources.

Crescent added assets through a $905 million acquisition of private E&P Ridgemar Energy in late 2024, complementing a smattering of other smaller transactions in the play.

Magnolia Oil & Gas has been a buyer in the more northern Austin Chalk play. The company added acreage in the storied Giddings Field through smaller M&A deals last year.

But the potential for large-scale M&A in the Eagle Ford this year is still relatively limited.

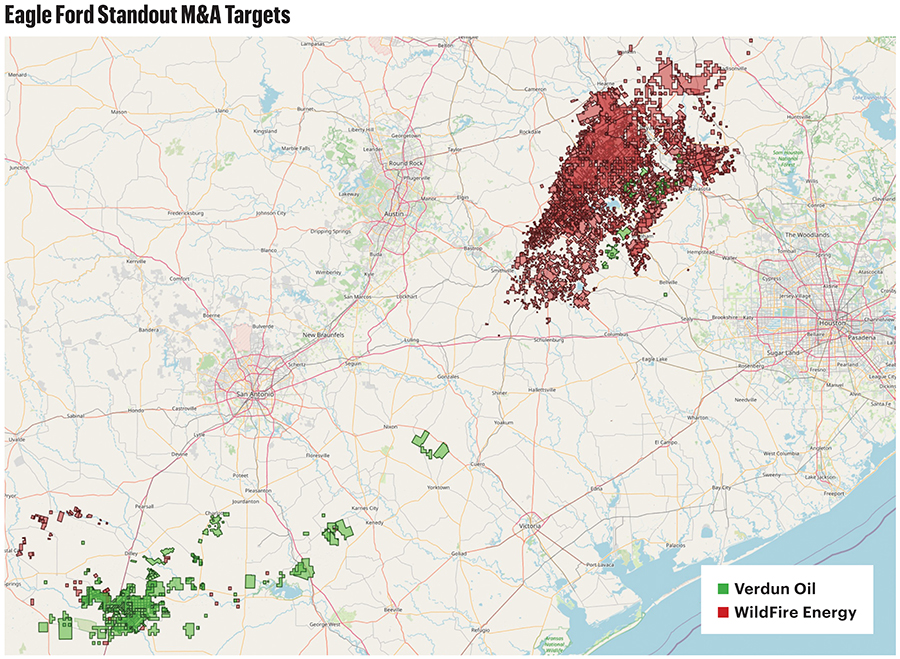

Standout targets remaining in the basin include Verdun Oil and WildFire Energy. WildFire has been another active buyer in the Austin Chalk, near Magnolia’s position.

Lewis Energy Group, a private operator in the Eagle Ford’s gas window, has been a seller recently. Last September, TotalEnergies announced acquiring a 45% stake in dry gas assets operated by Lewis.

Kimmeridge Texas Gas (KTG), a gas producer backed by investment firm Kimmeridge, also aims to grow through M&A in the Eagle Ford.

KTG had hoped to acquire SilverBow, one of its nearby neighbors. But those efforts were rejected—in a high-profile back-and-forth between Kimmeridge and SilverBow—when SilverBow agreed to the deal with Crescent.

RELATED

Recommended Reading

Halliburton Secures Drilling Contract from Petrobras Offshore Brazil

2025-01-30 - Halliburton Co. said the contract expands its drilling services footprint in the presalt and post-salt areas for both development and exploration wells.

E&P Highlights: March 3, 2025

2025-03-03 - Here’s a roundup of the latest E&P headlines, from planned Kolibri wells in Oklahoma to a discovery in the Barents Sea.

AIQ, SLB Collaborate to Speed Up Autonomous Energy Operations

2025-03-16 - AIQ and SLB’s collaboration will use SLB’s suite of applications to facilitate autonomous upstream and downstream operations.

Then and Now: 4D Seismic Surveys Cut Costs, Increase Production

2025-03-16 - 4D seismic surveys allow operators to monitor changes in reservoirs over extended periods for more informed well placement decisions. Companies including SLB and MicroSeismic Inc. are already seeing the benefits of the tech.

Diamondback in Talks to Build Permian NatGas Power for Data Centers

2025-02-26 - With ample gas production and surface acreage, Diamondback Energy is working to lure power producers and data center builders into the Permian Basin.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.