Gas-weighted assets’ M&A values have declined with gas futures since 2022, according to J.P. Morgan Securities analysis. (Source: Shutterstock.com)

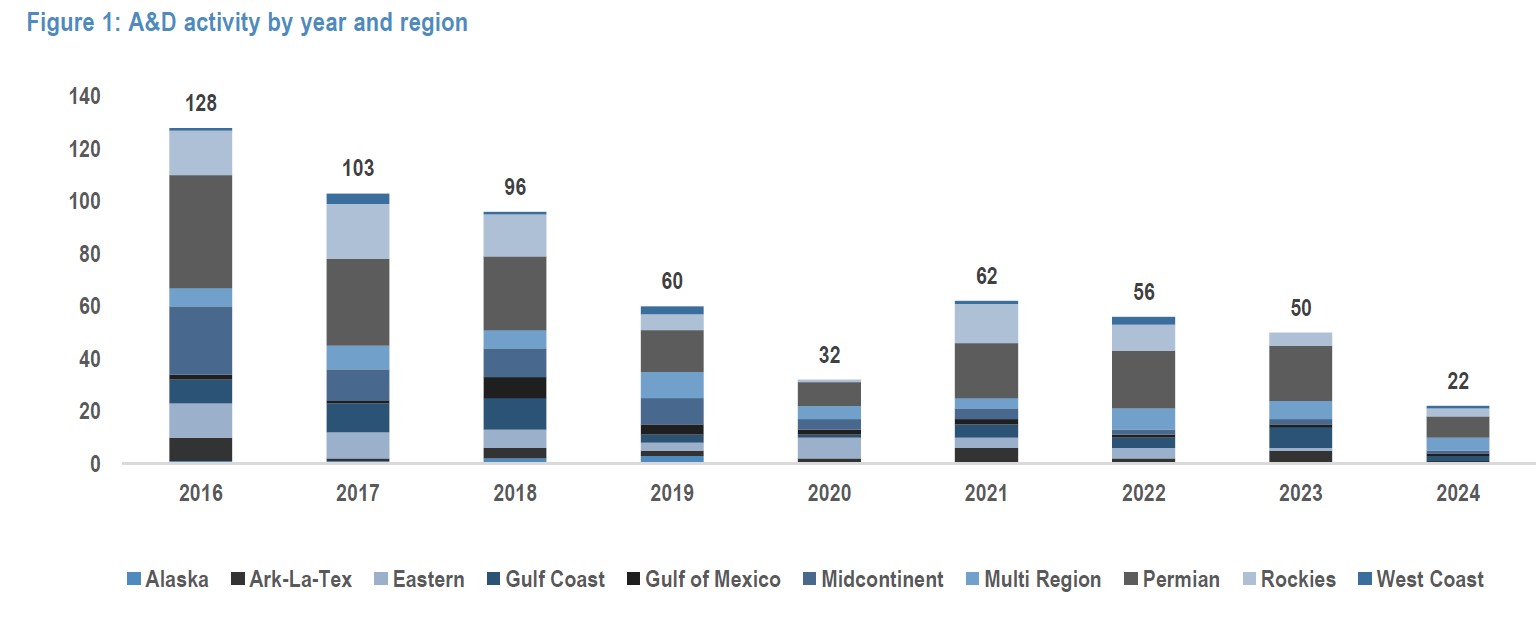

Permian Basin M&A remains the onshore Lower 48’s priciest market in terms of dollars paid per flowing barrels of oil equivalent per day, while values in all other regions have fallen this year, according to a J.P. Morgan Securities analysis.

In deals to date this year, including the $26 billion Diamondback Energy bid for the Midland Basin’s Endeavor Energy, the average winning offer is $38,398 per boe/d, analyst Arun Jayaram reported.

Jayaram reviewed deals valued at more than $100 million in Enverus’ database.

The 2024 price for Permian barrels and associated gas is up from an average $36,778 per boe/d in 2023, which included Exxon Mobil’s winning $59.5 billion bid for Midland Basin-focused Pioneer Natural Resources.

In Enverus’ Rockies region, which includes the Bakken and the Powder River and the Denver-Julesburg basins, values fell by 5%. Data show Rockies M&A values averaging $34,952 per boe/d value so far this year, down from $36,778 in 2023.

In the Midcontinent, which includes Oklahoma’s Anadarko Basin, values declined to $24,167 from $27,149, or 11%.

And the Gulf Coast, which includes the Eagle Ford, has received winning bids averaging $27,181 per boe/d, down a precipitous 41% from $36,694 in 2023.

The gas-weighted Ark-La-Tex area, which includes the Haynesville, has seen its value decline in step with gas futures. Deal values fell to $9,120 per boe/d so far this year compared to 2022’s $15,492. Natural gas spot prices rocketed in 2022 due to new European demand for LNG as a result of the start of Russia’s newest attempt to annex Ukraine.

More M&A underway

Overall, the average price paid this year per boe/d throughout the U.S., including Alaska and the Gulf of Mexico, has declined sharply to $30,364 per boe/d from the 2023 average of $35,109 and 2022’s $39,765, according to Jayaram’s analysis.

But more dealmaking is underway, he added.

“At the J.P. Morgan energy conference in mid-June, most E&P operators echoed expectations of further consolidation activity in the industry,” he reported.

Two major deals have been announced since the mid-June conference: SM Energy’s $2-billion bid for Uinta Basin-focused XCL Resources and Devon Energy’s $5 billion bid for Bakken-focused Grayson Mill Energy.

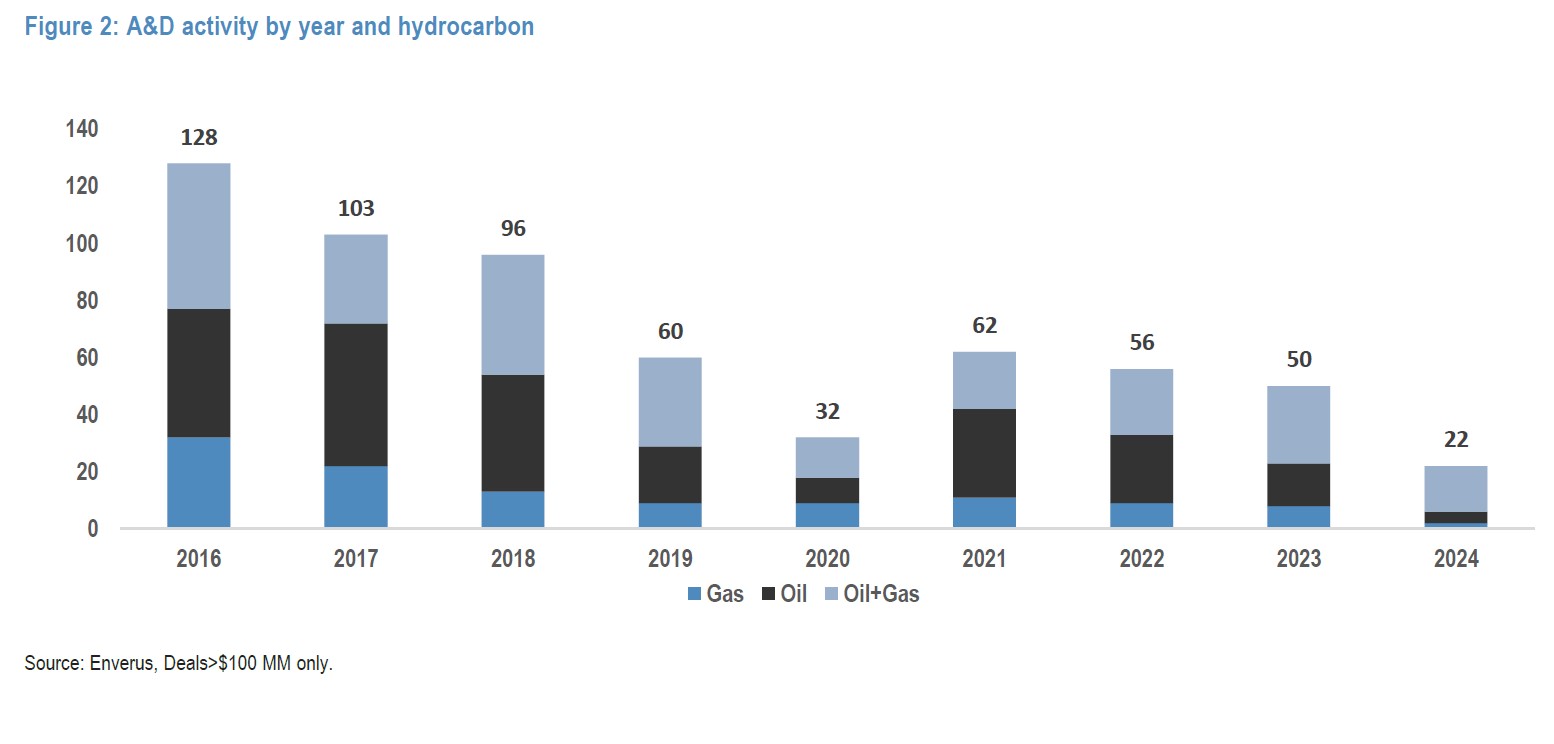

“An additional observation from our analysis is a decline in the mix of gas-focused transactions in 2024 vs. 2023 … while the share of ‘oil+gas’-focused transactions has increased in 2024,” Jayaram reported.

But 2024’s profile may be updated before 2025, he added. “We caveat these metrics by noting that deal activity trends may change as the year progresses.”

Recommended Reading

Biofuels Sector Unsatisfied with Clean Fuels Credit Guidance

2025-01-10 - The Treasury Department released guidance clarifying eligibility for the 45Z credit and which fuels are eligible, but holes remain.

Solar, Clean Energy Face Headwinds Amid Post-Election Uncertainty

2025-01-22 - With a new Trump administration taking charge, renewable energy, including solar, may face headwinds that stagnate project development or continue it at a slower pace, analysts say.

API’s Multi-Pronged Approach to Lower Carbon Operations

2025-01-28 - API has published nearly 100 standards addressing environmental performance and emissions reduction, which are constantly reviewed to support low carbon operations without compromising U.S. energy security.

Powerhouse: Enbridge Boosting Renewables, NatGas to Meet Surging Demand

2024-12-18 - As the need for clean and lower-carbon power grows, Enbridge is among the companies taking an all-of-the-above approach.

DOE Awards Two More Hydrogen Hubs Initial Funding

2025-01-22 - The awards were announced days before President Donald Trump directed federal agencies to pause disbursement of funds appropriated through the Infrastructure Investment and Jobs Act.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.