Upstream M&A activity fell sharply in the third quarter as public consolidation slowed and Permian Basin targets dwindled, according to Enverus Intelligence Research.

Upstream M&A activity slumped and transaction values fell to $12 billion in the third quarter as public consolidation paused and Permian Basin targets grew scarcer.

Third-quarter upstream dealmaking declined from more than $30 billion transacted during the previous quarter, according to data compiled by Enverus Intelligence Research (EIR). It was the lowest quarterly total since first-quarter 2023.

“Upstream M&A was bound to drop after the unprecedented lift of corporate mergers and private equity exits since 2023,” said Andrew Dittmar, principal analyst at EIR. “Those deals raised asset prices and cut the number of potential targets.”

The breakneck pace of public-on-public consolidation has left significantly fewer targets to pursue for acquisition. The market has seen $188 billion in public upstream company consolidation since the start of 2023, with 11 public deals topping $2 billion.

The biggest have included Exxon Mobil’s $60 billion acquisition of Pioneer Natural Resources, Chevron’s $55 billion acquisition of Hess Corp., and ConocoPhillips’ $17.1 acquisition of Marathon Oil.

Third quarter M&A scorecard

Transaction sizes were smaller than earlier in the cycle, but a handful of notable deals were inked in the third quarter.

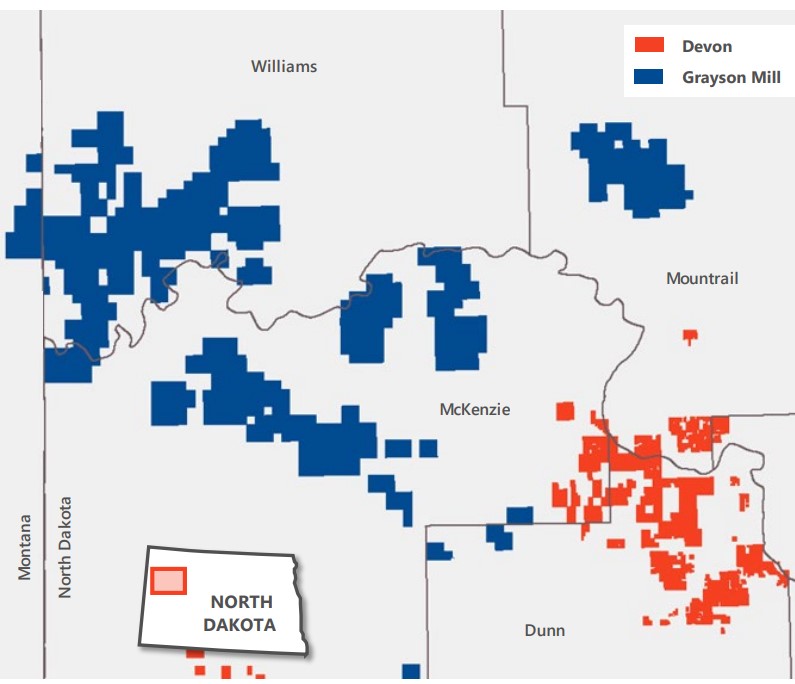

The largest M&A deal of the quarter was Devon Energy’s $5 billion acquisition of Grayson Mill Energy in North Dakota, which closed in late September.

The Grayson Mill deal transforms Devon’s business in the Williston Basin, adding over 300,000 net acres, 500 undrilled gross locations and 300 candidates for refrac projects. Most of the undeveloped locations are in the Bakken shale play, and about 20% are in the Three Forks interval.

EIR said basins such as the Williston and the Eagle Ford “offer the chance for buyers to get larger chunks of undeveloped inventory for less money per location, even if the inventory isn’t as economic to drill” as the core of the Permian Basin.

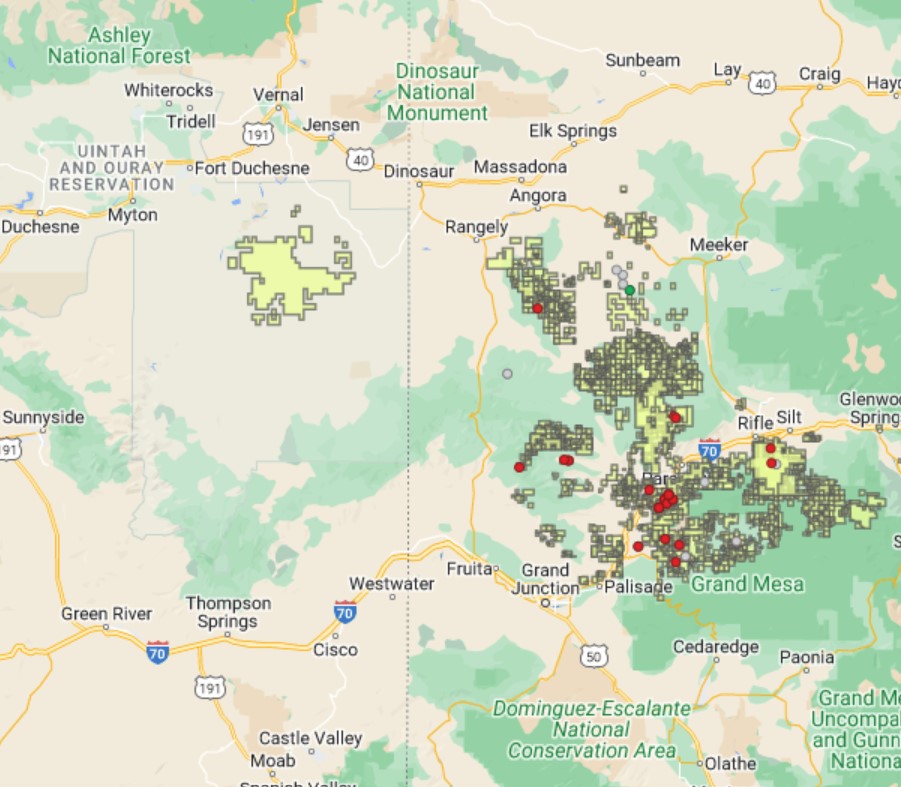

Private equity is also broadening its reach in basins with less competition than the Permian. Exhibit A: The $1.8 billion sale of Caerus Oil & Gas in Utah’s Uinta Basin and Colorado’s Piceance Basin to Quantum Capital Group—the second-largest deal in the quarter.

“There is still a significant amount of oil and gas to develop outside the main shale plays focused on by bigger public companies,” Dittmar said. “In some cases, like the Piceance Basin, the economics aren’t compelling to public companies that have higher-return drilling opportunities elsewhere.”

A newly formed Quantum portfolio company, QB Energy, will acquire and manage Caerus’ asset base in the Piceance Basin, where Caerus held around 600,000 acres. KODA Resources, an existing Quantum portfolio company, will acquire Caerus’ portfolio of approximately 160,000 acres in the Uinta Basin.

Permian gets challenging

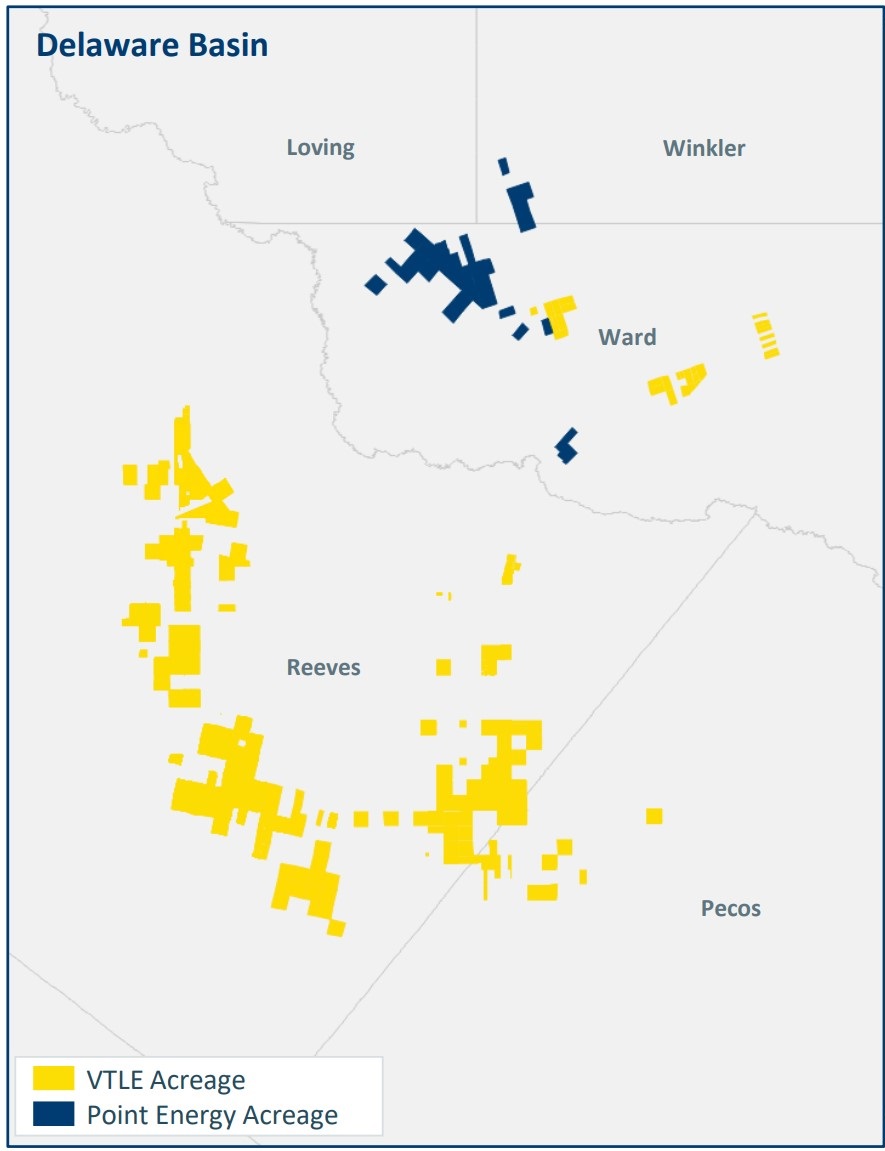

In the Permian, Vital Energy and Northern Oil and Gas’ (NOG) $1.1 billion acquisition of Point Energy Partners came in third among the quarter’s M&A deals.

Under the terms of the agreement, Vital acquired 80% of Point Energy’s assets, with NOG acquiring the remaining 20%.

The remaining opportunities for Permian acquisition are going to be challenging to buy for a reasonable price. Instead, buyers will pick up bigger chunks of middle-quality inventory or buy small pieces of high-quality rock “that go right to the front of the line for development,” Dittmar said.

Vital is adding 49 net (68 gross) drilling locations through the Point acquisition—not a huge incremental addition, EIR notes.

But the Point deal added inventory that’s competitive with the best rock Vital has left to drill, even if there wasn’t that much total inventory associated with the Delaware Basin asset, Dittmar said.

The fourth- and fifth-largest upstream deals of the third quarter were non-core asset divestitures by big spenders in last year’s M&A cycle.

APA Corp., parent company of Apache, completed a $950 million sale of conventional assets in the Permian’s Central Basin Platform to an undisclosed private buyer.

In April, APA closed a $4.5 billion acquisition of Callon Petroleum, deepening its horizontal portfolio in the core of the Permian.

After closing a $12 billion acquisition of private Permian E&P CrownRock, Occidental Petroleum has similarly been on a divestiture campaign to shore up its balance sheet.

During the third quarter, Occidental sold Barilla Draw assets in the southern Delaware Basin to Permian Resources for about $818 million.

RELATED

After M&A, Some ‘Stingy’ E&Ps Plan to Hold Operated Shale Inventory

Dusting off the maps

While corporate M&A has slowed, consolidation in the upstream industry is far from over, Dittmar said.

“If you look out a few years from now, there are going to be fewer companies operating in the main U.S. shale plays,” he said. “However, the path to get there may be a bit bumpier from this point.”

Going forward, buyers might need to offer higher premiums than the average 15% being paid out to selling companies to lure remaining M&A targets into a sale.

EIR also expects non-core asset sales to continue playing a prominent role in the upstream A&D market. Companies that were buyers are now likely to sell parts of the combined portfolio.

Future non-core sales could target fringier and lower-quality Permian plays, the Midcontinent and areas like the Uinta Basin, where Ovintiv has reportedly considered selling assets.

Assets in western Oklahoma and the Permian’s Northwest Shelf might not have the well economics or scale to interest the big publics—but they’ll draw interest from private companies and smaller public players.

WildFire Energy and Verdun Oil in the South Texas Eagle Ford shale also remain notable private M&A opportunities.

“Now that the big shale plays are increasingly consolidated, the industry is dusting off maps and rediscovering areas that have been under the radar for the last decade,” Dittmar said.

RELATED

Recommended Reading

Williams to Invest $1.6B for On-Site Power Project with Mystery Company

2025-03-07 - Williams Cos. did not name the customer or the location of the power project in a regulatory filing.

FERC Reinstates Permit for Williams’ Mid-Atlantic Project

2025-01-27 - The Federal Energy Regulatory Commission’s latest move allows Williams’ Transco natural gas network to continue operations after a D.C. court shot down the expansion plan.

Williams Commissions Two NatGas Projects to Expand Transco Network

2025-04-01 - Midstream company Williams Cos. added to its network capacity in the southern U.S. with the commissioning of the Southeast Energy Connector and the Texas to Louisiana Energy Pathway.

Williams’ CEO: Pipeline Permitting Costs Twice as Much as Steel

2025-03-12 - Williams Cos. CEO Alan Armstrong said U.S. states with friendlier permitting polices, including Texas, Louisiana and Wyoming, have a major advantage as AI infrastructure develops.

DC Circuit Denies Rehearing for Williams’ Mid-Atlantic Project

2025-01-23 - Williams Cos.’ Regional Energy Access will continue operating as the midstream company seeks an emergency FERC certificate to keep supplying natural gas to Pennsylvania, New Jersey and Maryland.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.